Q1 2026 - In Review

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

Mark Twain

The quote from Mark Twain is a reminder that our perception often drives our reality. We see what we’ve conditioned ourselves to see. History serves as a guide but it cannot be a road map for the future. We recognize patterns or similarities and extrapolate them into some vision of what lies ahead. Taken to extremes, what we think is reality is merely a construct of our imagination, filled with confirmation biases to support an argument that we wear like a badge of honor. The financial news media loves it. Bad news out? Bring in the perma-bear to tell us why we should run for cover. The worst is yet to come. Good news? Bring in the perma bull who will argue that the good times can roll on forever. The viewer’s emotional DNA will cling to the pundit who feeds his inner pessimist or optimist. Hearing an expert argue something in your emotional hemisphere rings that truth even more true. Investing over a long period time is really a mathematical formula. Over the short term, investing becomes trading and trading becomes a battle of fear and greed, with fear often winning in the end.

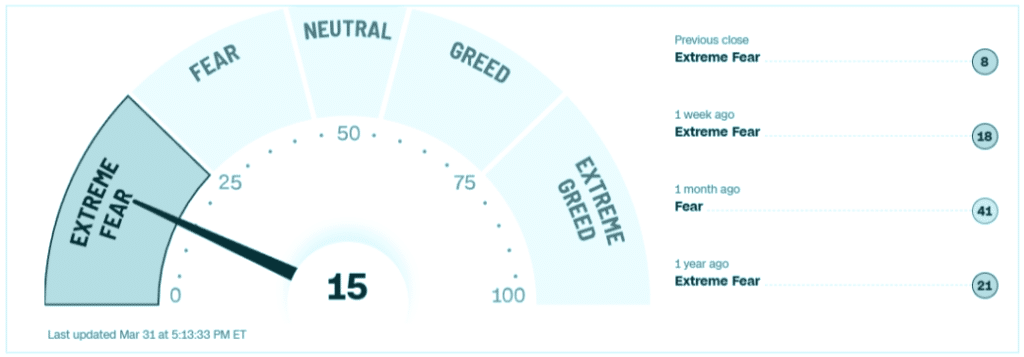

At the end of March, investors were in a fearful mood, evidenced by the chart below from CNN [1].

Given the unrest in the middle east, skyrocketing oil prices, and talk of a resurgence in inflation brought an end to the goldilocks period we had post Liberation Day. Extreme fear and greed are contrarian indicators. The fear is usually worse than reality and thus a good time to invest and the promise of good times forever can be a reminder to reflect and make sure you haven’t swallowed all the Kool Aid.

Despite this poll, if you look at the pending Initial Public Offering (“IPO”) of SpaceX, you’ll likely witness extreme greed. The valuation being thrown around is $2 trillion [2]. That is $2 with a T against roughly $20 billion in revenues this year. SpaceX’s valuation implies, jokingly, a monopoly on space. It is a topsy turvy world.

The numbers.

As we get into the meat of earnings season for the first quarter, earnings growth the companies in the S&P 500 are estimated at a little more than 17% over Q1, 2025. For Q2 through Q4 2026, analysts are calling for growth rates of 19.1%, 21.2%, and 19.3%, respectively. For the year, they are predicting 17.4% growth in earnings. That implies a forward earnings ratio (“PE”) of 19.8, which, while high by historical standards, stands comfortably below the forward PE ratio of 22 at the end of December 2025 [3]

Interest rates were thought to be going lower again this year, but after the Iranian war started and oil prices surged, the probability of two, ¼ % cuts evaporated and was replaced by a slight chance of an increase. [4]

Bond yields typically decline when equities decline, or there is a higher risk of recession. Not so this time. Inflation isn’t good for bonds. Nor are large government deficits and uncomfortably high national debt levels. Those seem to be trumping any flight to bonds during turbulent times.

Gold, which sold off materially from its all-time high of $5,327.65 per ounce in late January to roughly $4,600 per ounce by the end of March seems inconsistent considering the geopolitical tensions [5]. Given how much it had appreciated over the past 24 months, it was due for a pullback. As gold surged, it seemed to bring in all the gold bugs from under every rug to tell the masses that it was all because of the worthless nature of paper money. Gold bugs have been calling or the end of paper money, or fiat currency, since fiat currency was issued in the 17 th century in Europe [6]. It certainly highlights some important issues, like runaway deficits and ballooning debts. The world has a debt problem. Gold is but one offramp. The narrative on gold has been the narrative for decades, but once the bull market began in earnest, the narrative fit the chart beautifully. It will take a long time to upend the US dollar as the world’s reserve currency. With the digitization of money, maybe that timeline will come quicker. In the meantime, the global financial market is so embedded with greenbacks, that an overnight unwind of it seems to be a low probability event.

Given the structural deficits, growing global government debts, and ever-increasing geopolitical conflicts, gold can be an important component of a diversified portfolio.

Short Term Risks Create Long Term Opportunities.

As we enter month two of an effectively closed Strait of Hormuz, economic problems continue to mount. Even if we open the Strait tomorrow, the lag in getting oil refiners up and running, unloading oil and LNG from buoyed ships, it will take months, not weeks to get things back to normal. And that isn’t counting the unknown loss of production and refining from the region that was part of the flow of legitimate, unsanctioned energy. Feedstocks for fertilizer and chemicals for semiconductors are also prevented from reaching their end-markets. The opportunity lies in the ability to stay patient. To look beyond a few quarters and see that the world has a vested interest to open the strait, installing new rules and moving forward. The global economy will have to accept one truth; that no one country can go it alone.

Portfolio Positioning.

We continue to remain focused on credit quality and less sensitive to changes in interest rates in our fixed income holdings. Early in an economic cycle, or after extreme fear, is the time to take on higher credit and interest rate risk. In the current environment, we reaming cautiously positioned. We continue to hold gold, and infrastructure outside of our normal equity holdings. We also increased our international exposure in the first quarter. We remain at the lower end of our risk models, having raised cash after selling down some of our equity holdings in the last quarter of 2025. The cash will be redeployed when we see an opportunity to do so. Until then, the cash cushion has served us well in recent months.

References

A Values-Based Approach, Customized to You

There’s no one-size-fits-all strategy. Whether you’re passionate about renewable energy, gender equity, or local community development, we work with you to build a portfolio that honors your values while staying aligned with your long-term financial goals.

As fiduciaries and long-term partners, we take great care in selecting investment options that reflect both your priorities and your needs. We’re committed to ongoing research, transparent reporting, and evolving with you as your values or goals shift.

Want to learn how your investments can make a difference?

Let’s talk about how your financial plan can reflect your personal convictions.