Q3 2025 Update

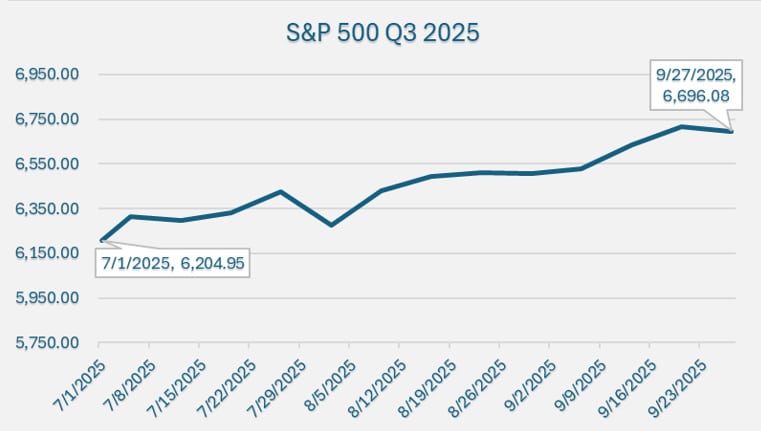

Q3 was a continuation of where Q2 left off; a steady march higher for equities and fixed income. As Liberation day faded from memory, investors were able to digest the data and breathe a collective sigh of relief as some of the worst fears surrounding tariffs did not come to fruition. The US Dollar stabilized and moved slightly higher in the quarter, but was still down nearly 10% for the year. Gold continued to move higher, reaching all-time highs on an inflation-adjusted basis. International developed market equities gained but at a much slower pace but still remain comfortably higher than the US markets year-to-date. US Small and Mid-Cap equities were able to reverse their earlier losses, with small caps, gaining major ground in the month of August.

| Index (ETF Proxy) | Q1 | Q2 | Q3 | YTD |

|---|---|---|---|---|

| S&P 500 | -4.28 | 10.91 | 8.09 | 6.16 |

| S&P MidCap 400 | -3.75 | 3.69 | 5.48 | -0.20 |

| S&P SmallCap 600 | 7.55 | 12.29 | 9.09 | 20.77 |

| MSCI EA FE | 7.55 | 12.29 | 4.84 | 26.61 |

| US Aggregate Bond | 2.76 | 1.21 | 2.04 | 6.13 |

| Gold | 19.20 | 5.43 | 16.25 | 46.10 |

| US Dollar | -3.94 | -7.04 | 0.93 | -9.87 |

The S&P 500 consensus estimate for earnings per share for 2025 stands at approximately $267.65 per share, up from $264.21 in Q2, which equates to a multiple of 25 times. For 2026, earnings are estimated to be $304 per share up slightly from Q2, implying a forward multiple of earnings of 22 times. These estimates imply an earnings growth rate of roughly 10.5% for 2025 and 13.5% for 2026 vs the long-term average of roughly 9.5%. The only sector estimated to have negative earnings growth is energy.1

Tariffs. The administration has made some headway. The table below provides a concise summary of where things stand, but as we all know, things can change in an instant. The president is using all the tools at his disposal to re-write global trade. With many deals, there are exceptions. Certain goods are exempt. Other deals come with strings such as agreements to build production capacity in the U.S. It is difficult to stay on top of all the changes. The uncertainty is still there but, for the most part, the worst seems to be behind us. Markets in general like certainty. “Just tell us what the rules are and we will adjust. This uncertainty is not healthy for anyone.” The world is inherently uncertain but constantly moving the goal posts adds another layer that we’d rather avoid.

The president’s negotiating style has been chaotic. He wrote a book about it. Ask for the sun when you only wanted the moon. When the other side agrees to the moon, they think they’ve negotiated successfully.

| Country/Region | Date (2025) | Type of Tariff Action | Brief Description |

|---|---|---|---|

| China | Aug 12, 2025 | Tariff truce extended | 90-day extension of U.S.-China tariff truce (avoids hike from 30% to 145%) |

| India | August 27, 2025 | Tariff increase to 50% | U.S. imposes an additional 25% tariff on most Indian imports (now totaling 50%) |

| European Union | Jul 27, 2025 | Trade deal | U.S.-EU deal averts 30% tariff; imposes 15% on most EU goods + EU $600B U.S. investment |

| Canada | Jul 10, 2025 | Tariff increase to 35% | U.S. raises tariff on Canadian imports from 25% to 35% (some USMCA goods exempt) |

| Mexico | Jul 31, 2025 | Tariff truce extended | U.S. grants Mexico 90-day reprieve on planned 30% tariff amid ongoing talks |

| Japan | July 22, 2025 | Trade deal (15% Tariff) | U.S.-Japan trade agreement: 15% tariff (down from 25% threat) + ~$550B Japanese investment |

| Brazil | Jul 9, 2025 | Tariff increase to 50% | U.S. imposes 50% tariff on Brazilian imports (up from 10%), amid political dispute with Brazil |

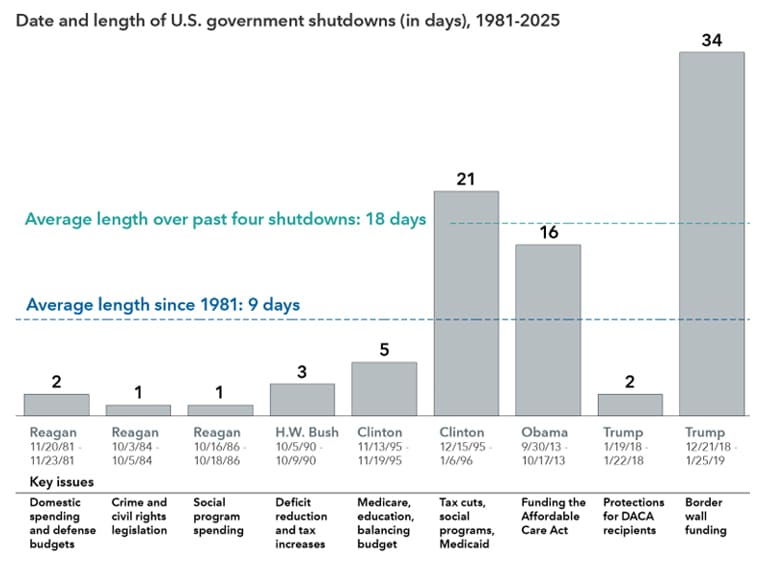

The US Government Shutdown is unfortunately nothing new. We have been here before. The issues at play are always different. In this instance, it is mostly about entitlements. The democrats want to maintain the Affordable Care Act (“ACA”) subsidies and remove the clauses in the recent spending bill that raise certain requirements for Medicare. Social Security taxes are also in play.

Government workers may be permanently let go rather than temporarily furloughed. Certain economic data will be delayed and certain measures like employment may be distorted for a short period of time once the government is back to work. For the most part, shutdowns have little effect on the economy. Both parties are walking a fine line, as any cuts to government employees or departments may have a direct impact on the polls in next year’s congressional mid-term elections.2

The AI Revolution – Boom or Bust. Technological progress is happening at the fastest pace in human history. As with any technology, there are two phases. The first phrase is invention and disruption. Advances in technology usher in a wave of disruption where industries that once dominated are pushed to the side in favor of the new entrants. The second phase is where mass adoption of these innovative technologies takes hold. One cohort believes the ubiquity of these changes will happen overnight. The other believes it will happen much later. This juxtaposition creates an interesting market dynamic. The stock market is a discount machine. In a mix of math and emotion, it settles on valuations intended to represent the total value of future profits into the present. Since the future is unknown, and the new, burgeoning industries poised to lead us into the future have not yet won, investors are left to add their own collective wisdom on what that value should be. It is the mix of optimism and a calculator that moves markets.

Front and center of this AI revolution is the increasing complexity of silicon and what man has been able to do with it. Semiconductor chips have been getting smaller and faster. We can process information that was thought impossible a decade or two ago. Special machines are required to produce leading edge chips. Those chips allow people to gather and analyze data of every kind. We need servers, data centers, wiring, electricity, and teams of highly educated people to sift through this treasure trove of data to bring new products and services to the masses. We are firmly in phase one. Phase two is what will drive most of the productivity gains. One set of firms invents these recent technologies and the rest find a way to use them. Phase two, and when it starts to materialize, is what will move markets again. What we cannot pinpoint with mathematical certainty is when this mass adoption will happen. If phase two comes later than what is baked into stock prices, they will falter. As with every other technological leap in the past, there will be a collective optimism that turns to over optimism, but progress will come.

How does one take stock in all of this and how are we invested? As we have stated many times, return expectations always factor in the risk taken. Avoiding unnecessary risks is always paramount. Our benchmark is the US Total Stock Market Index, the MSCI International Index and the US Aggregate Bond Index. Where we have deviated from our benchmark slightly is our fixed income holdings. We have a little less than half of our fixed income investments outside the aggregate bond index, which results in slightly less interest rate exposure and less credit exposure. We exited our high yield dedicated fund holdings in Q3 and have funds that “may” have a portion of their assets in high yield. This allows the manager to increase or decrease the credit risk it is taking without being “stuck” with a mandate to always be invested in high yield. International equity exposure has always been a cornerstone of our portfolio holdings. We added a fund dedicated to infrastructure that has roughly two thirds of its holdings outside the U.S.

A Values-Based Approach, Customized to You

There’s no one-size-fits-all strategy. Whether you’re passionate about renewable energy, gender equity, or local community development, we work with you to build a portfolio that honors your values while staying aligned with your long-term financial goals.

As fiduciaries and long-term partners, we take great care in selecting investment options that reflect both your priorities and your needs. We’re committed to ongoing research, transparent reporting, and evolving with you as your values or goals shift.

Want to learn how your investments can make a difference?

Let’s talk about how your financial plan can reflect your personal convictions.